Credit Score Ranges – Everything You Need to Know

Introduction

In the world of personal finance, a credit score Ranges are a numerical representation of an individual’s creditworthiness.

Understanding credit score ranges is crucial, as it directly impacts one’s ability to secure loans, credit cards, and favorable interest rates.

In this comprehensive guide, we will delve into everything you need to know about credit score ranges, what constitutes a good credit score, and the factors that influence your financial health.

The Basics of Credit Score

What is a Credit Score?

A credit score is a three-digit number that reflects an individual’s creditworthiness, providing lenders with insights into their ability to manage credit responsibly. It is based on an individual’s credit history and various financial behaviours.

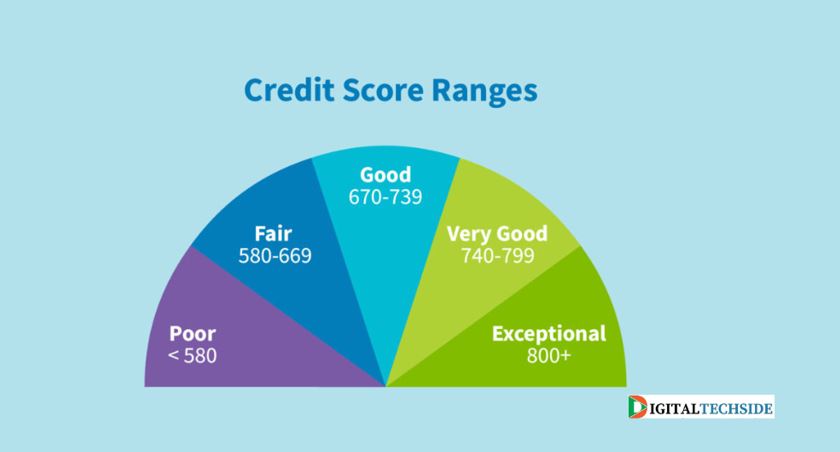

Credit Score Ranges

1. 300–579: Poor

Individuals in this range may face challenges in obtaining credit and, if approved, may encounter higher interest rates. Poor credit may result from missed payments, defaults, or bankruptcy.

2. 580–669: Fair

A fair credit score suggests some financial responsibility, but individuals may still encounter limitations in accessing credit or may face higher interest rates.

3. 670–739: Good

A good credit score indicates a reliable credit history, making individuals eligible for most credit products. They are likely to qualify for favorable interest rates.

4. 740–799: Very Good

A very good credit score reflects a strong credit history, making individuals eligible for the best interest rates and favorable credit terms.

5. 800–850: Excellent

An excellent credit score positions individuals as low-risk borrowers, making them eligible for the most favorable terms and offers on credit products.

What Constitutes a Good Credit Score?

1. Access to Credit:

A good credit score provides individuals with access to a wide range of credit products, including credit cards, loans, and mortgages.

2. Favorable Interest Rates:

Individuals with a good credit score are likely to qualify for lower interest rates, resulting in reduced overall borrowing costs.

3. Quick Loan Approvals:

Lenders are more inclined to approve loans quickly for individuals with a good credit score, reflecting a positive credit history.

4. Higher Credit Limits:

Individuals with good credit scores may receive higher credit limits on their credit cards, providing greater financial flexibility.

Factors Influencing Credit Scores

1. Payment History:

Timely payments on credit accounts positively impact credit scores, while late payments, defaults, or bankruptcies have adverse effects.

2. Credit Utilization:

The ratio of credit used to the total available credit, known as credit utilization, influences credit scores. Lower utilization is favorable.

3. Length of Credit History:

A longer credit history is generally viewed positively, as it provides a more comprehensive picture of an individual’s credit management.

4. Types of Credit in Use:

A mix of credit types, such as credit cards, installment loans, and mortgages, contributes positively to credit scores.

5. New Credit Accounts:

Opening multiple new credit accounts in a short period of time may negatively impact credit scores, as it can be seen as a sign of financial distress.

Monitoring and Improving Credit Scores

1. Regularly Check Your Credit Report:

Review your credit report regularly to identify inaccuracies or fraudulent activities that may affect your credit score.

2. Pay Bills on Time:

Timely payment of bills is crucial for maintaining a positive credit history and a good credit score.

3. Manage Credit Responsibly:

Use credit responsibly, avoid maxing out credit cards, and maintain a healthy credit utilization ratio.

4. Limit New Credit Applications:

Limit the number of new credit applications to avoid potential negative impacts on your credit score.

Conclusion

In conclusion, understanding credit score ranges is essential for individuals seeking financial stability and access to credit.

A good credit score opens doors to favorable interest rates, higher credit limits, and quicker loan approvals. Monitoring and managing credit responsibly are key to maintaining or improving credit scores over time.

By incorporating positive financial habits and staying informed about credit scores, individuals can enhance their financial health and make informed decisions when it comes to borrowing and managing credit.

If you have specific concerns about your credit score, it’s advisable to consult with credit experts or financial advisors to receive personalized guidance tailored to your financial situation.

FAQ’s (Frequently Asked Questions)

Q1: How often should I check my credit score?

Ans: It is advisable to check your credit score at least once a year. You can obtain a free credit report from major credit bureaus annually.

Q2: Can my credit score change?

Ans: Yes, credit scores are dynamic and can change based on your financial behavior, payment history, and other factors.

Q3: How long does it take to improve a credit score?

Ans: Improving a credit score is a gradual process. Positive financial behaviors over time, such as timely payments, can contribute to improvement.

Q4: Can I get a loan with a bad credit score?

Ans: While it may be challenging, individuals with bad credit scores can still access loans, though they may face higher interest rates.

As a DIGITALTECHSIDE author, the majority of our articles have been focused on technology, blogging, business, lifestyle, social media, web design and development, e-commerce, money, health, education, entertainment, SEO, travel, and sports.

Contact us at digitaltechside@gmail.com if you have questions of anything.